Thread Starter

#1

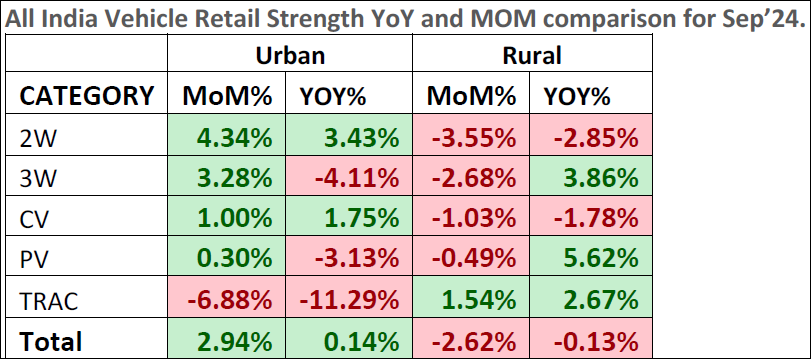

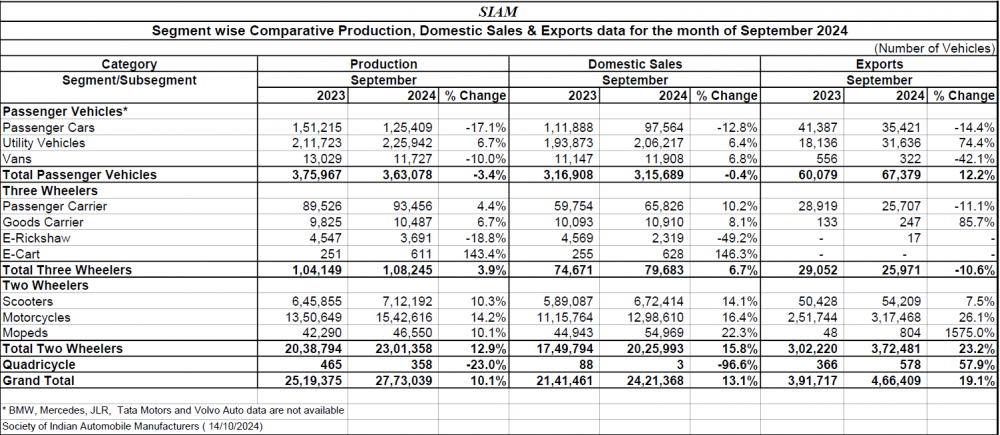

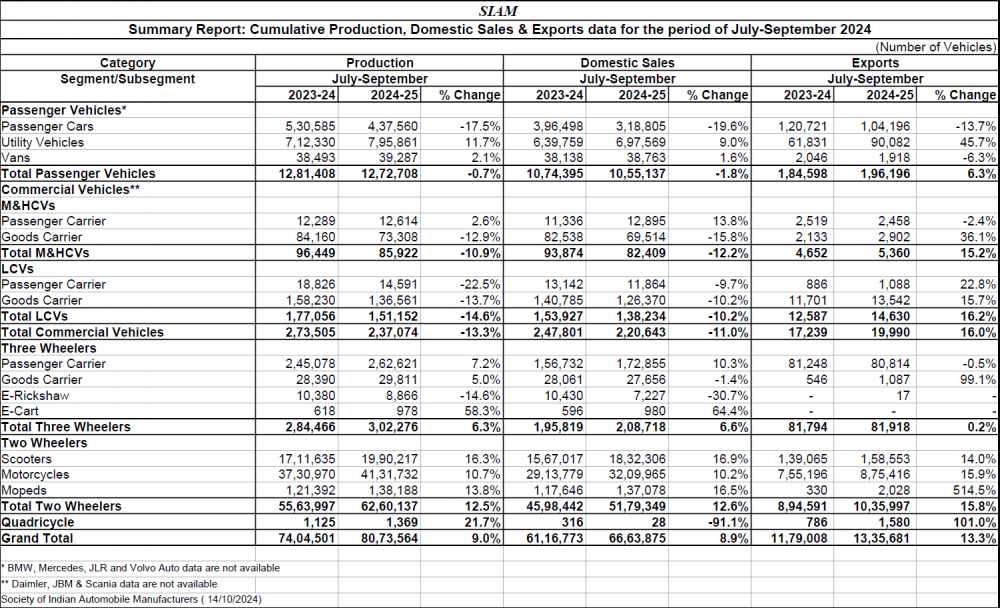

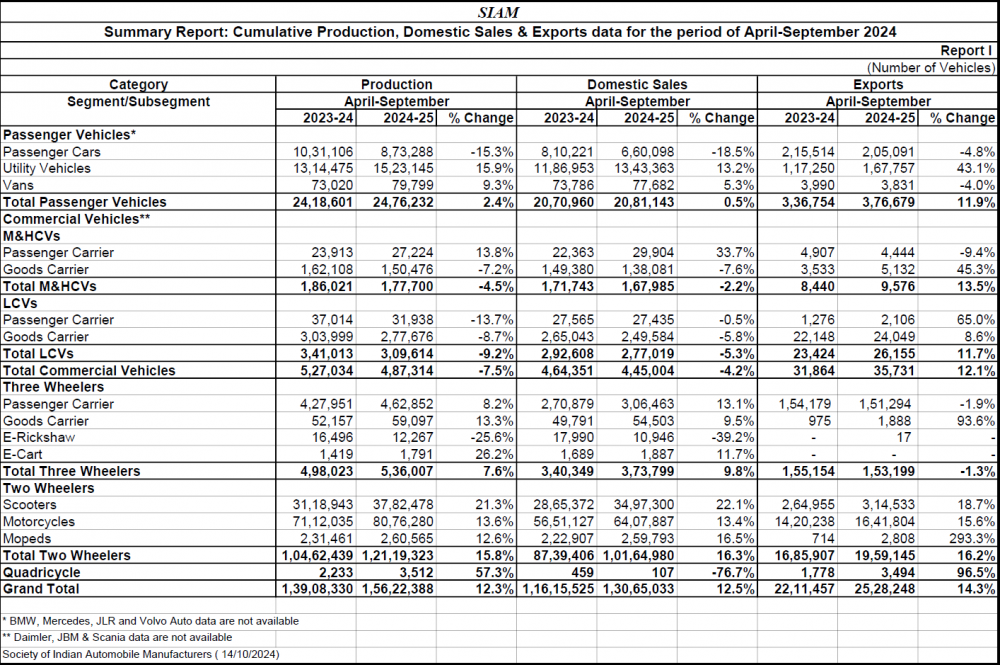

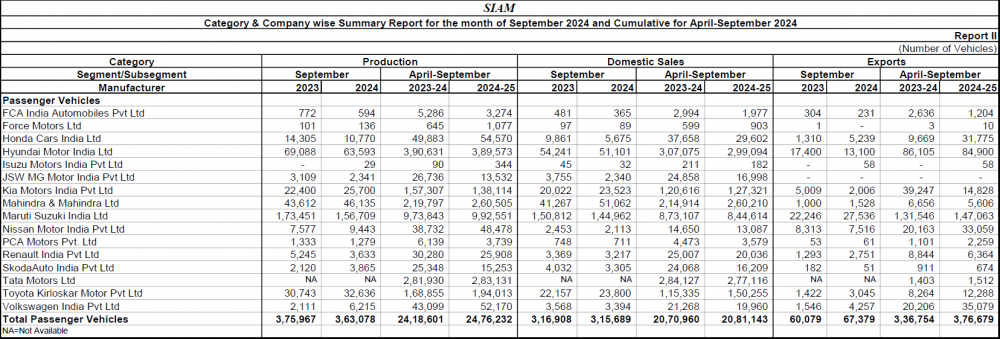

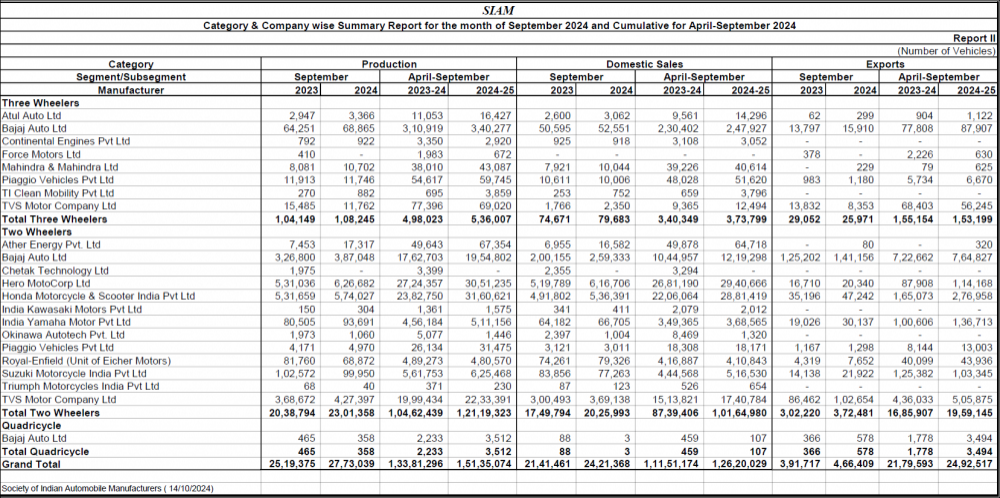

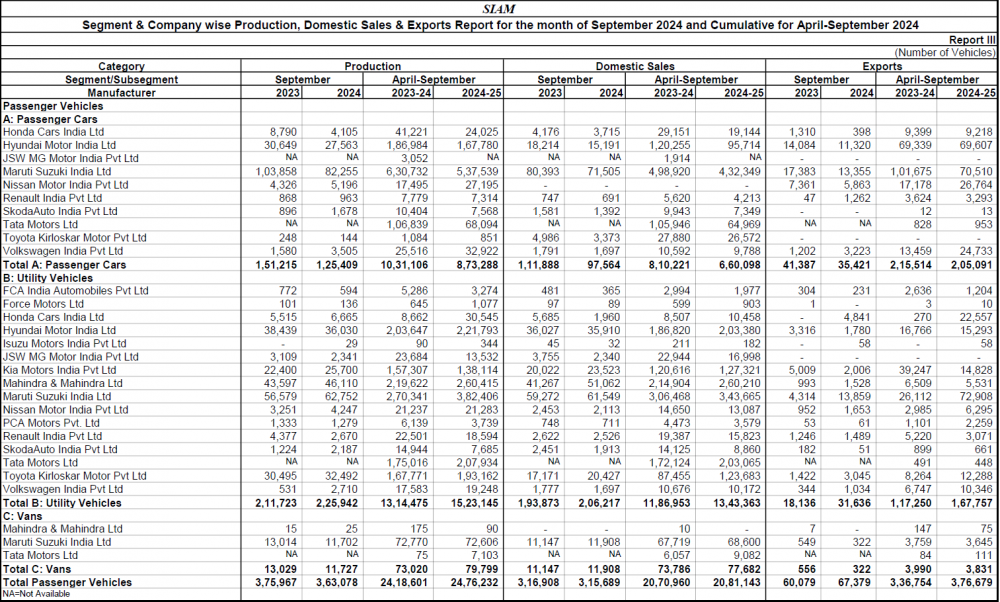

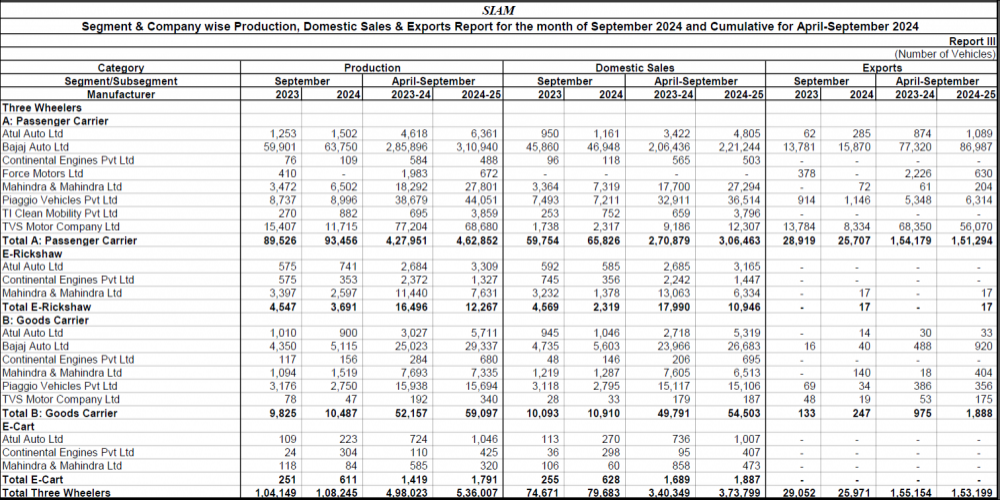

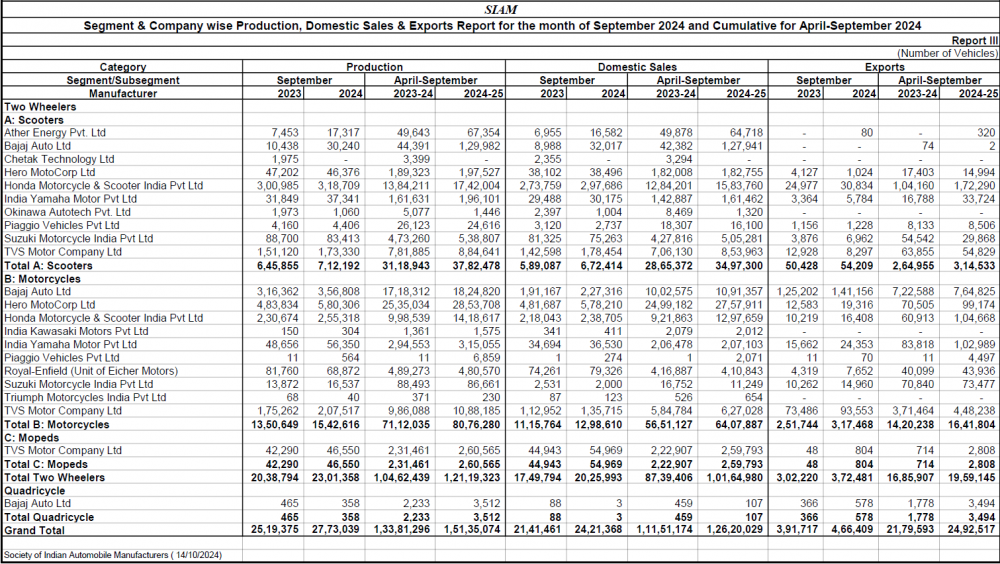

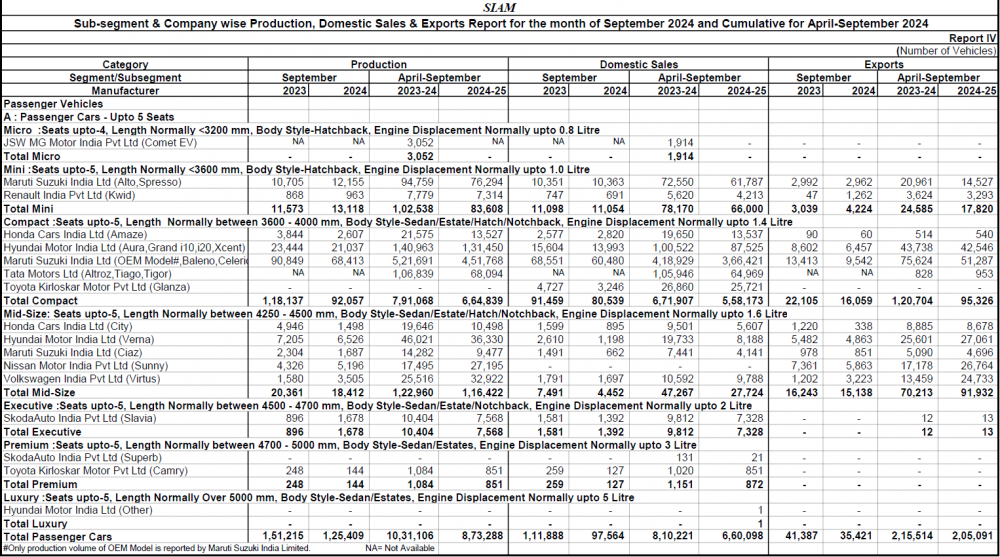

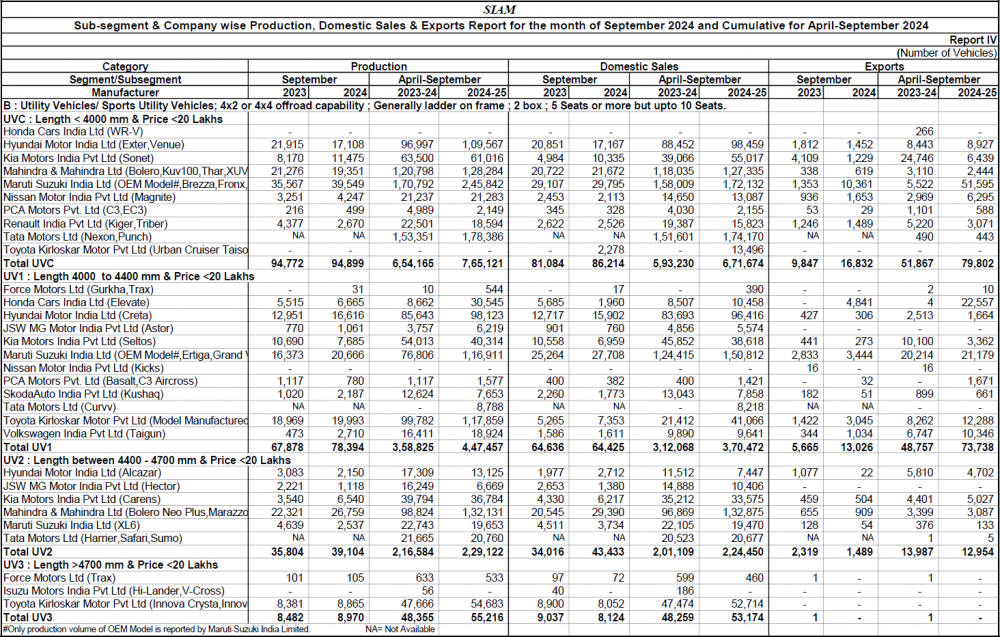

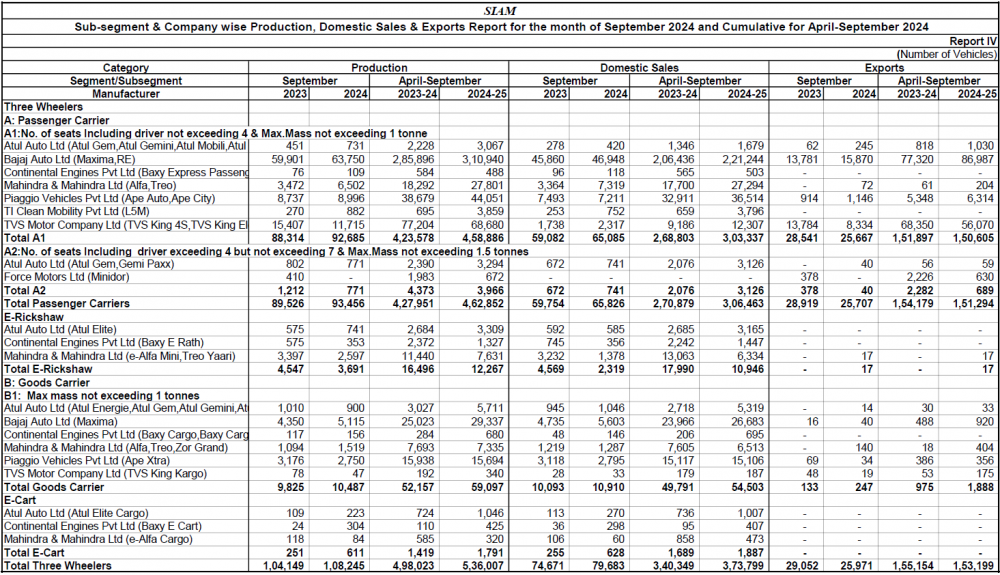

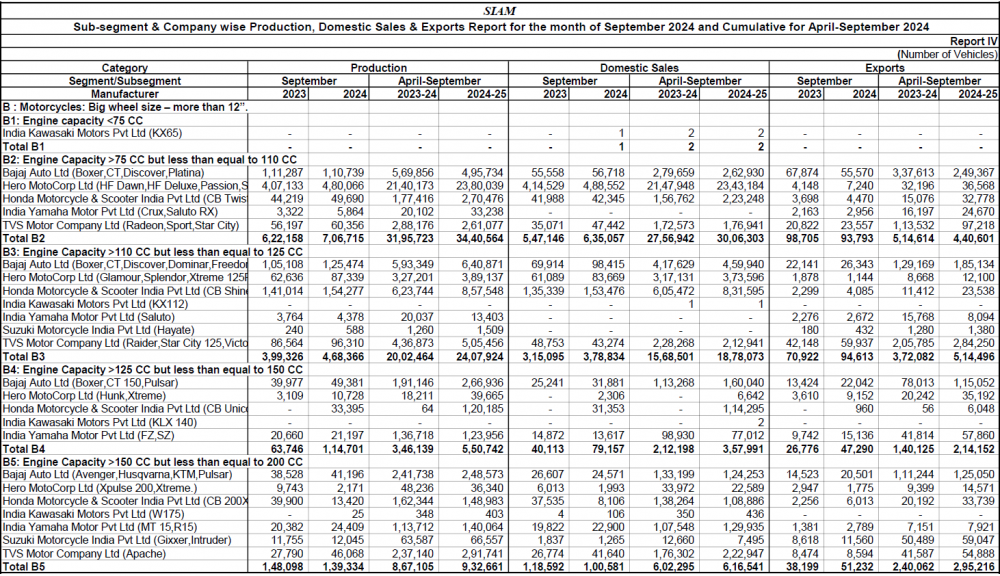

September 2024 Indian Car Sales

Top 10 Selling Cars: September 2024

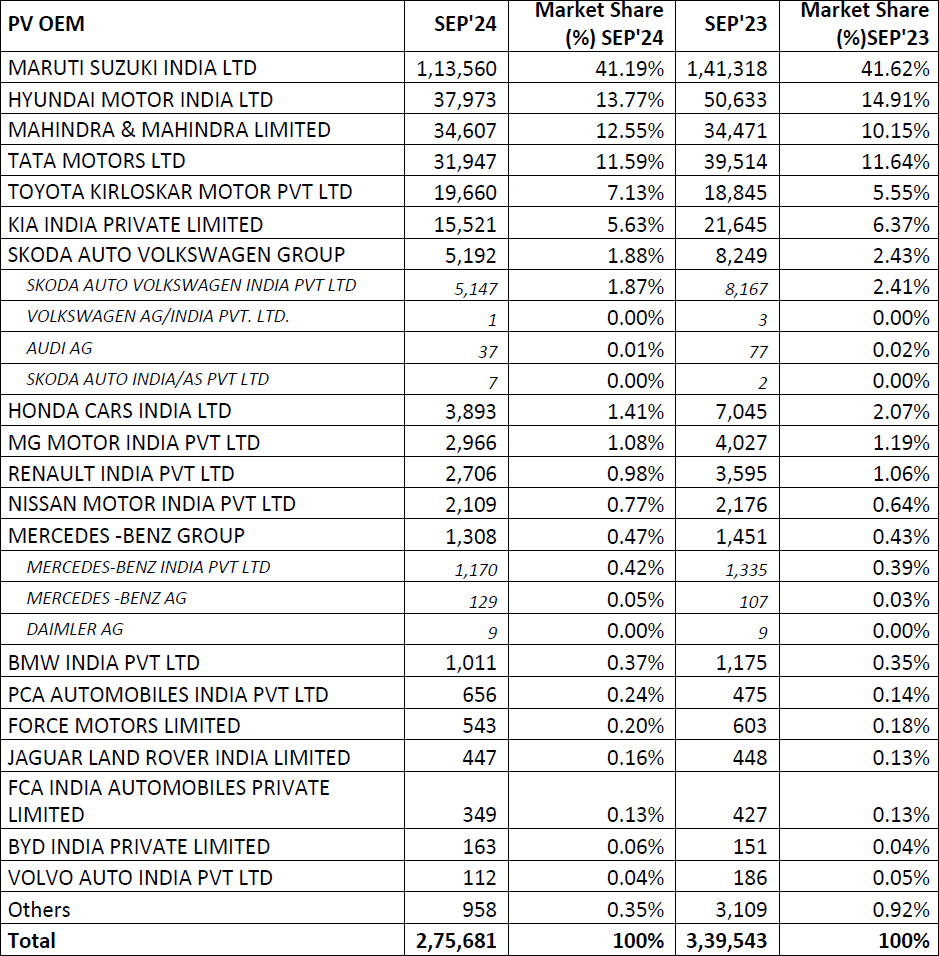

Manufacturers' Market Share: September 2024

Citroën September 2024 Indian Car Sales

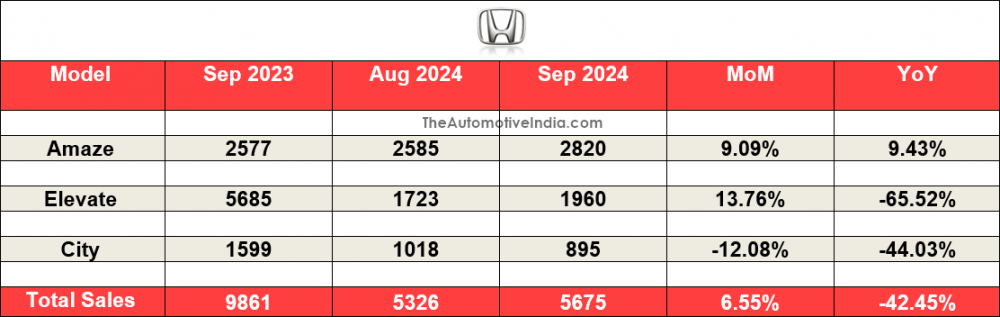

Honda September 2024 Indian Car Sales

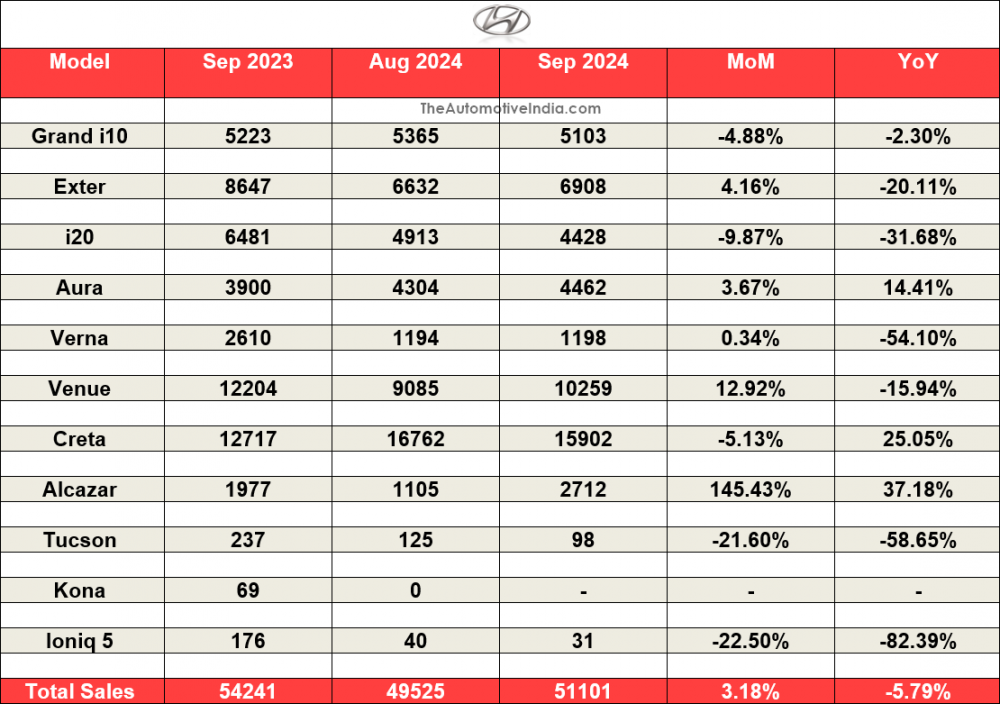

Hyundai September 2024 Indian Car Sales

Jeep September 2024 Indian Car Sales

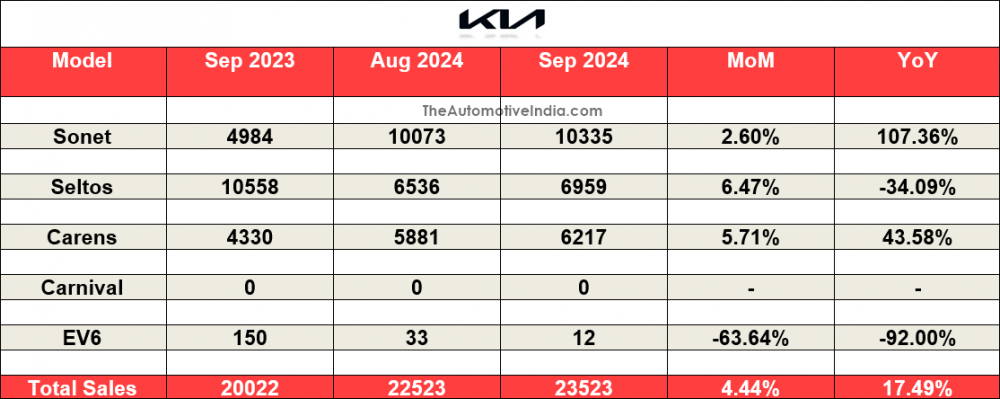

Kia September 2024 Indian Car Sales

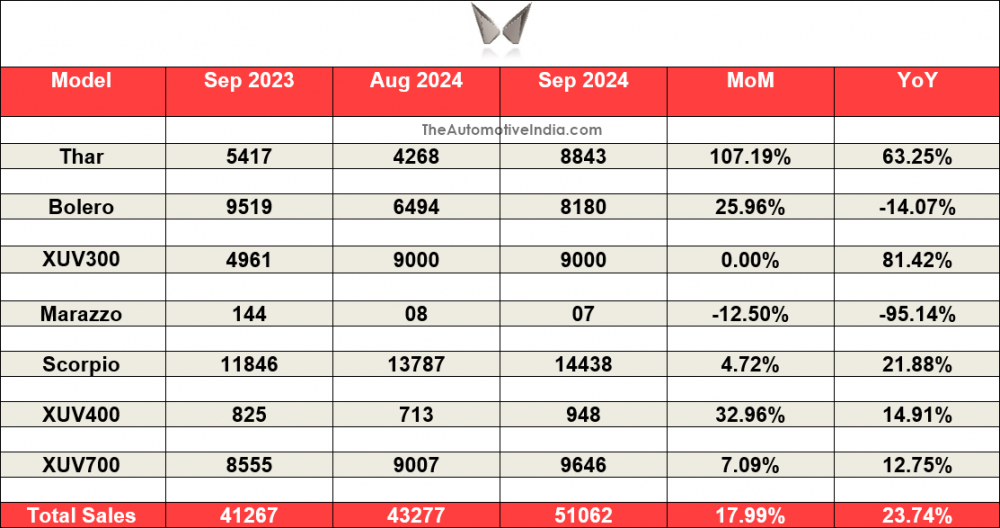

Mahindra September 2024 Indian Car Sales

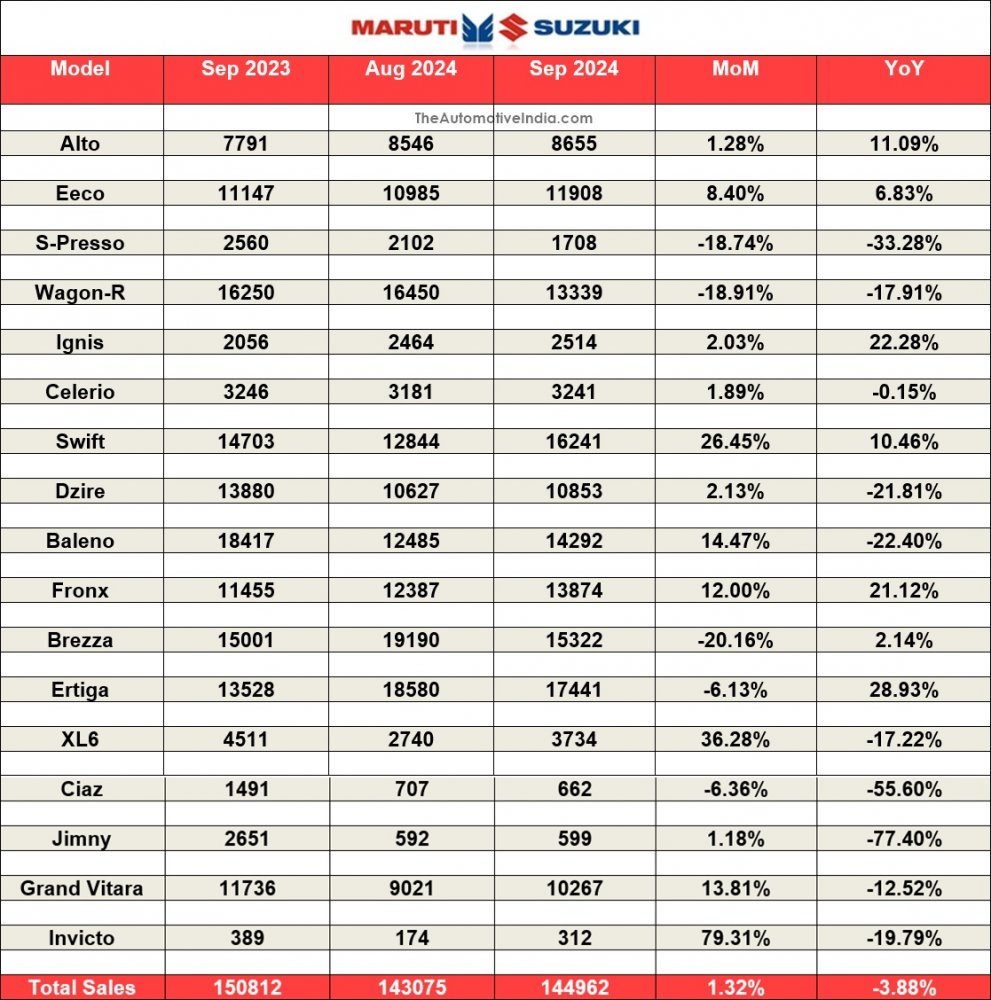

Maruti Suzuki September 2024 Indian Car Sales

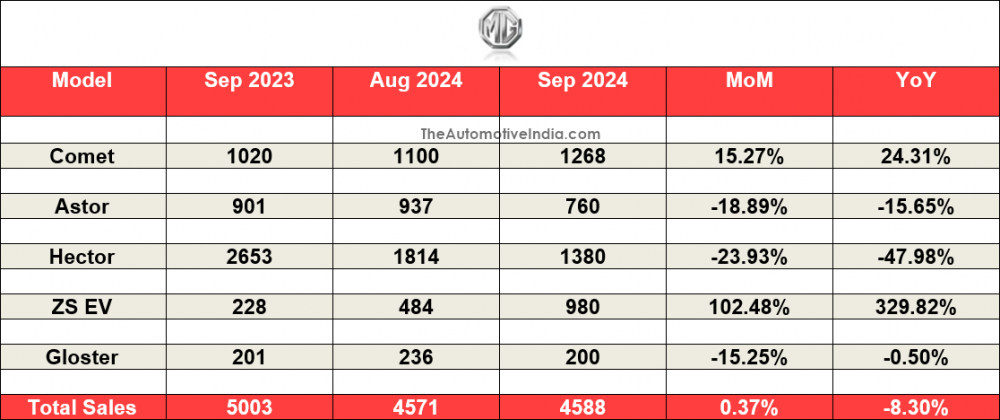

Morris Garages September 2024 Indian Car Sales

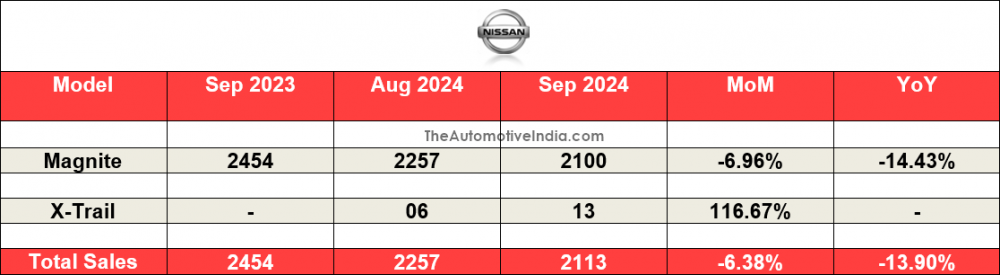

Nissan September 2024 Indian Car Sales

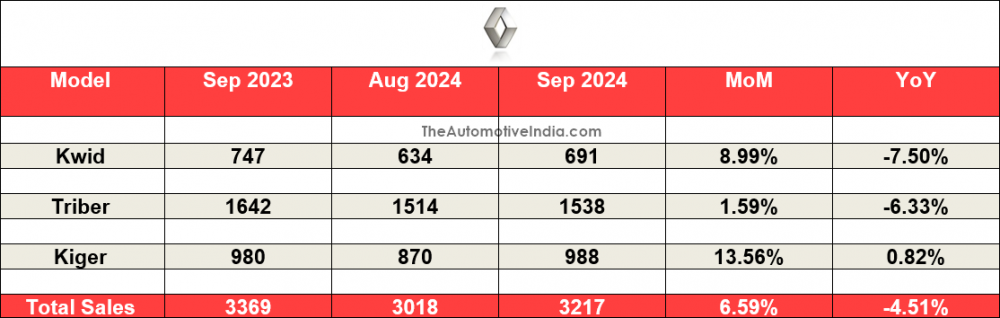

Renault September 2024 Indian Car Sales

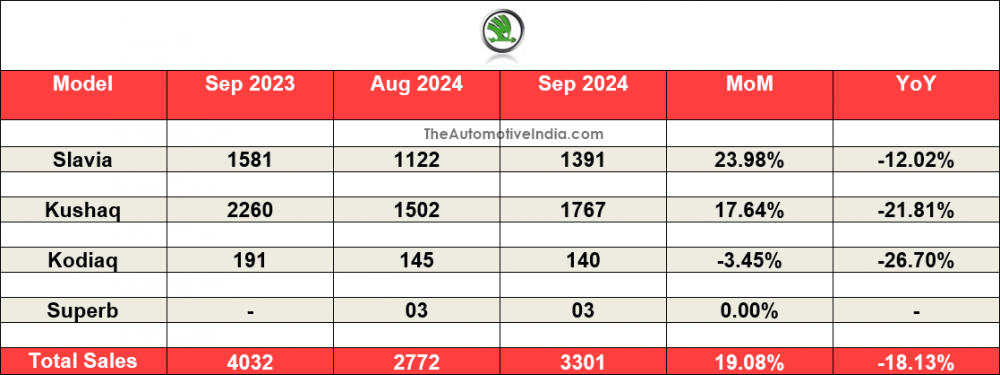

Skoda September 2024 Indian Car Sales

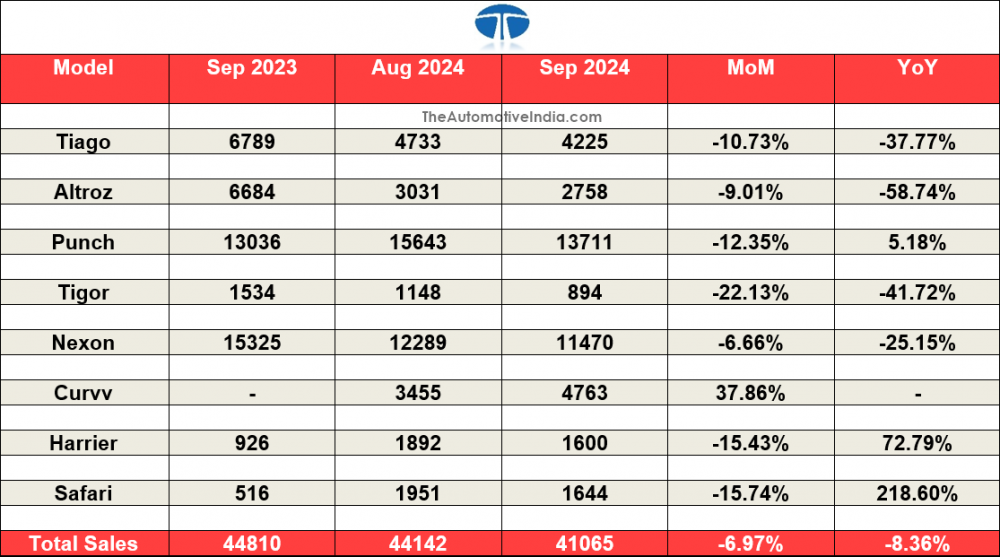

Tata Motors September 2024 Indian Car Sales

Toyota September 2024 Indian Car Sales

.

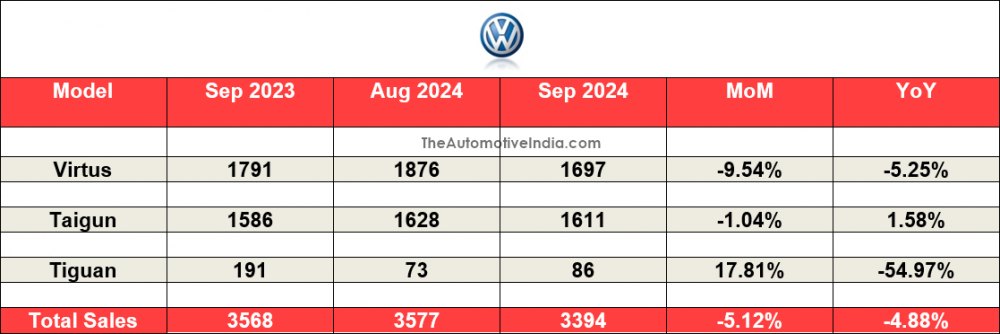

Volkswagen September 2024 Indian Car Sales

Top 10 Selling Cars: September 2024

Manufacturers' Market Share: September 2024

Citroën September 2024 Indian Car Sales

Honda September 2024 Indian Car Sales

Hyundai September 2024 Indian Car Sales

Jeep September 2024 Indian Car Sales

Kia September 2024 Indian Car Sales

Mahindra September 2024 Indian Car Sales

Maruti Suzuki September 2024 Indian Car Sales

Morris Garages September 2024 Indian Car Sales

Nissan September 2024 Indian Car Sales

Renault September 2024 Indian Car Sales

Skoda September 2024 Indian Car Sales

Tata Motors September 2024 Indian Car Sales

Toyota September 2024 Indian Car Sales

.

Volkswagen September 2024 Indian Car Sales

Drive Safe,

350Z